Plan and Budget 2021/22

Welcome to FSCS's Plan and Budget. Here you can read the most recent issue and browse back issues from the past five years.

FSCS Plan and Budget 2021/22

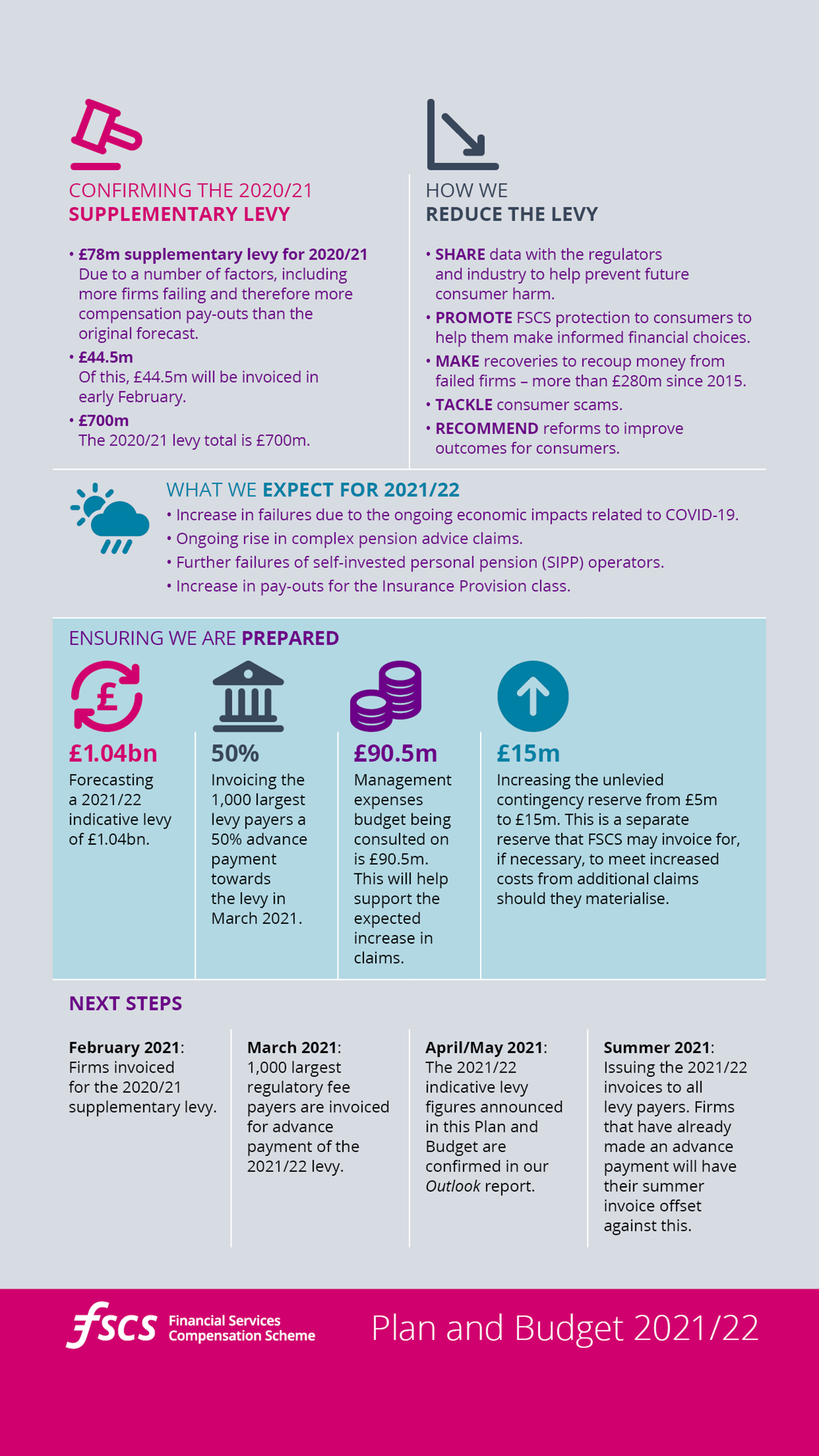

Plan and Budget confirms the 2020/21 supplementary levy and forecasts the 2021/22 compensation costs and levy.

Chief Executive’s introduction

Watch this short video to see FSCS Chief Executive Caroline Rainbird introducing Plan and Budget.

The highlights from Plan and Budget

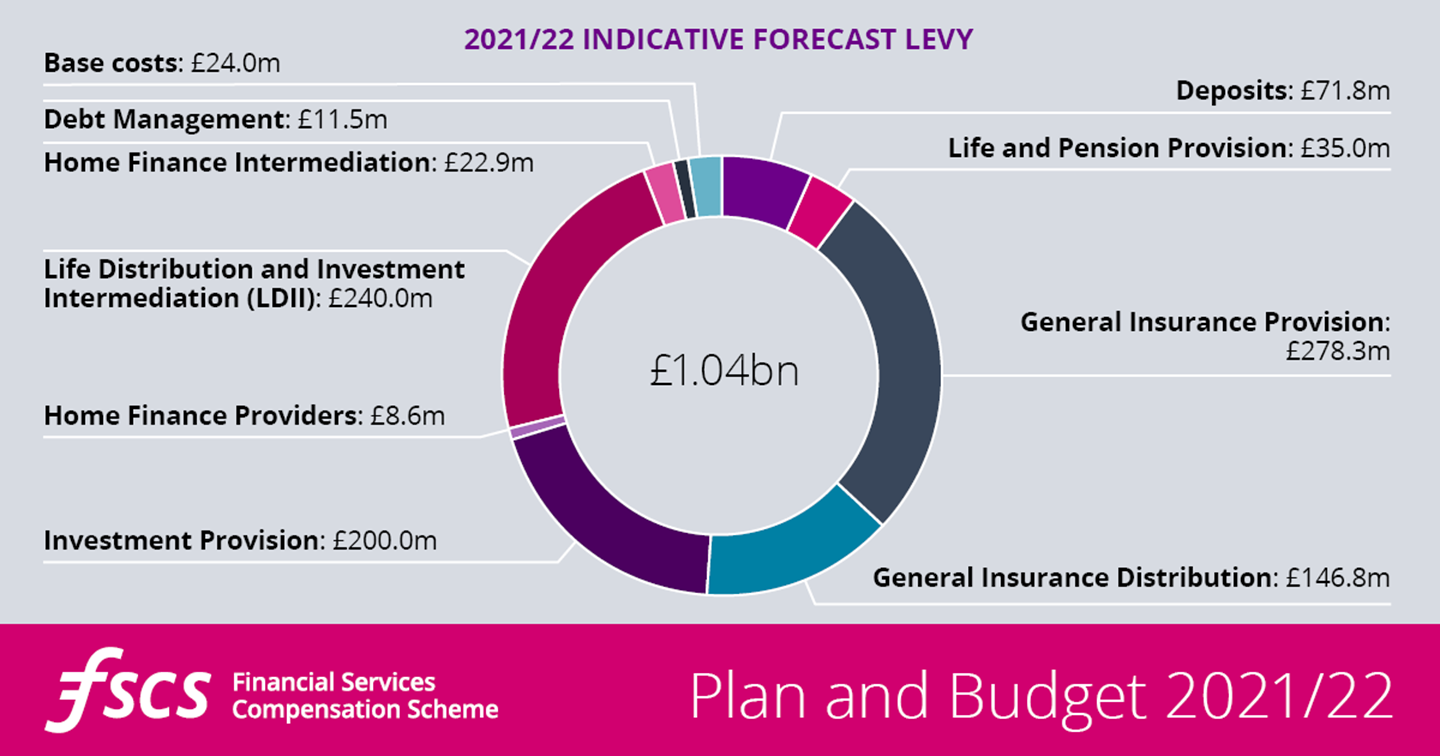

Breakdown of the 2021/22 indicative levy

Plan and Budget is available in different languages, as well as in braille, large print, and as a recording.

Older editions of Plan and Budget are available in our Plan and Budget archive.