Deposit takers course

Our free deposit takers course has been designed for bank, building society and credit union staff.

Completing the course will enable you to confidently advise your customers, by gaining a greater understanding of the protection we can provide.

Key topics covered

- What FSCS is and why it's important.

- The protection FSCS provides to your customers.

- Levels of compensation and the claims process.

- Why you must prominently display FSCS information.

There's also an eLearning version that will play on your PC/laptop. If you're unsure how to install the download, ask your IT team.

Deposit protection Q&As - banks and building societies

- The bank or building society must be authorised by the Prudential Regulation Authority (PRA).

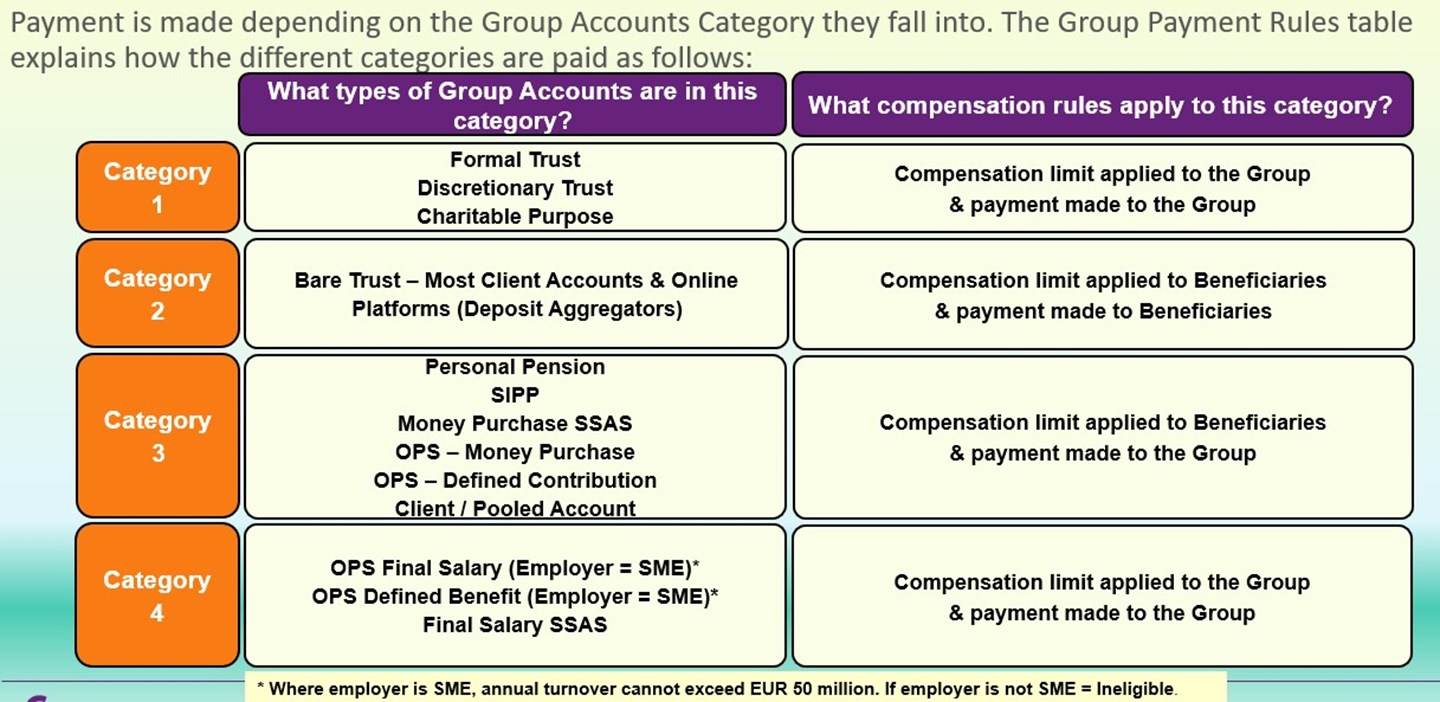

- In certain cases, the account holder(s) determines the protection limit that applies and how that applies. For example, the way a trust is set up means different limits might apply.

- Protection is across all accounts held within the bank/banking group, not per account.

- The customer does not have to live in the UK for FSCS protection to apply but the bank or building society must be UK authorised.

- If a bank or building society fails, FSCS will automatically pay back customers’ money within seven working days in most cases. FSCS always aims to get customers their money back as soon as possible.

- Reimbursements for temporary high-balance claims and accounts where the beneficial owner of the funds is not obvious (for example, where monies are held under trust arrangements) can take up to three months.

Group accounts